Differentiate your hedge through interest rate differentials

For Swiss investors, the current and unprecedented low level of domestic interest rates has dramatically raised the costs of hedging foreign currency risk. Because these vary between currency pairs, one may be tempted to capitalize on such differences and design a hedging strategy that optimizes costs for a set level of risk. We investigate the merits and characteristics of such a strategy over the past 20 years, a period featuring many different interest rates configurations. Our results highlight the importance of considering the implicit exposure to exchange rate moves and allow us to put forth optimal market conditions for the performance of such a strategy.

The strategy

Laying the groundwork With this motivation in mind we set out to evaluate the performance of such a hedging policy over the past 20 years. Taking the perspective of a Swiss based investor we simplified the currency exposure to the US dollar and the Euro – by far the largest allocations in a typical portfolio of foreign assets. The relative weights were set to 60% for the US Dollar and 40% for the Euro.

We selected as a benchmark the common policy described above, hedging at all times 50% of the exposure to both the US Dollar and the Euro. In terms of risk reduction, this means that only half of the volatility of both currency pairs is passed through to the investor’s portfolio when translated into the Swiss franc. In terms of hedging costs, half of the interest rate differentials for both currency pairs is periodically deducted from the value of the portfolio.

Beyond static

Our strategy was designed to be more flexible. Every week we measured the volatility of the benchmark’s returns over the previous two years. We did the same for all possible combinations of hedge ratios for the two currency pairs, by increments of 10% (for example, starting with a 0% hedge ratio for the USDCHF and the EURCHF, then 0% for the USDCHF and 10% for the EURCHF, and so on until we reached 100% for both currency pairs, yielding 11 x 11 combinations every week). To ensure an acceptable level of risk, we discarded all the combinations resulting in a more volatile hedging strategy than our benchmark. Finally, we retained only the one associated with the lowest hedging cost.

Performance analysis

Hedging costs are material The first graph shows the cumulative performance of the benchmark (in blue) and the strategy (in red). The first thing we notice is their downward trend, caused by two distinct effects.

Firstly, the US dollar and the Euro have both been losing ground to the Swiss franc over our sample (-39% and -28% respectively). Because both policies are only partially hedged at a given time, they haven’t been able to completely offset this effect and must absorb part of the ensuing losses. Secondly, and as has been described earlier, hedging costs money to a Swiss investor. Indeed – and apart from rare exceptions – the interest rate differentials for both the USDCHF and EURCHF currency pairs have been constantly in negative territory for our whole sample. As a result, the benchmark hedging policy loses -27.4% over the period. The strategy does a bit better with -22.2%, which translates into an annualized outperformance of 0.35%.

Searching for (risky) yield

In order to gain a better insight into the strategy’s performance, we plot in green its cumulative added value over the benchmark for the whole period. This corresponds to the red line minus the blue line in the previous graph. This layout highlights different performance regimes for the strategy: there are times when it increases steadily (for example: 2002 to 2004, 2006 to 2008 and 2017 to 2020), and others when it drops sharply (2008 to 2010 and early 2015).

The signs of « carry »

These performance patterns are often associated with carry strategies, where one borrows in one currency with low interest rates (e.g. the Japanese yen) and invests the sum in a currency with higher interest rates (e.g. the Australian dollar), cashing in the difference between the income and cost streams.

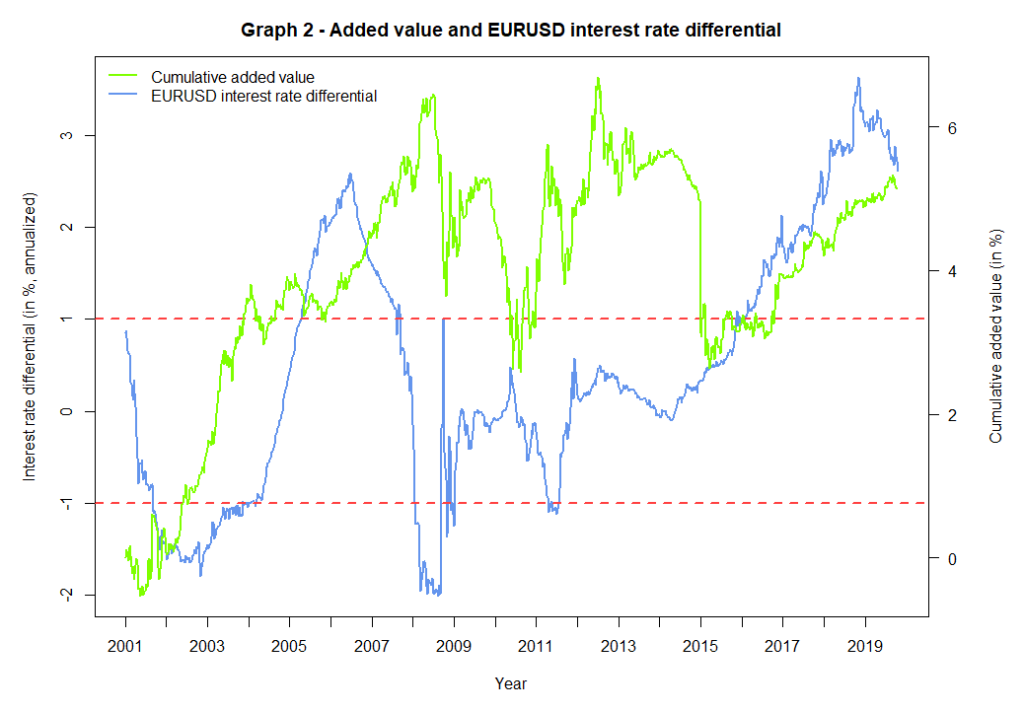

A changing opportunity set

Coming back to the periods when the strategy performs particularly well (2002-2004, 2006-2008 and 2017-2020), we see that they coincide with periods when the EURUSD interest rate differential was material (i.e. outside the -1% / +1% band delimited by the two dashed horizontal lines). In these periods it seems the hedging costs we hope to save by varying the hedge ratios away from the benchmark warrant the risk taking.

Looking deeper under the hood

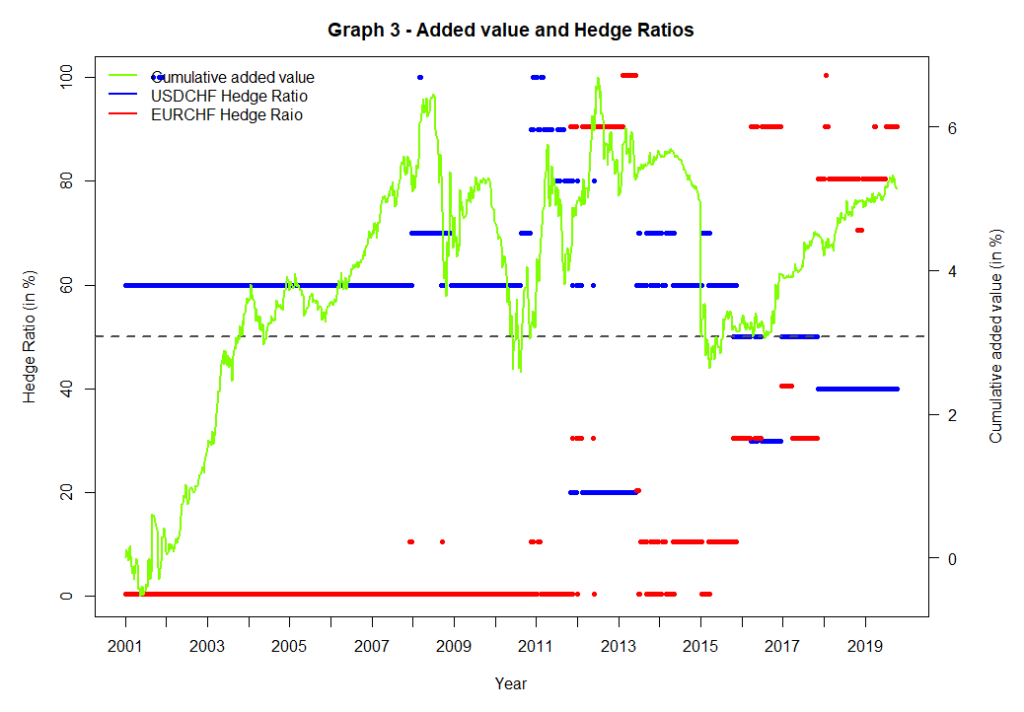

With the strategy outputs presented so far, we’ve been able to highlight some of its behavioral patterns but have been left with educated guesses as to why these occur. In the coming paragraphs, we go a step further and investigate the strategy’s deviations from the benchmark in terms of hedge ratios. Remember that the benchmark is stuck with 50% hedge ratios for both the USDCHF & EURCHF over the whole period. Hence, when the strategy’s hedge ratios differ from 50%, it means it is taking a tactical position. A hedge ratio of 70% for the USDCHF for example means that the American currency is over-hedged with respect to the benchmark by 20%. All of this information is featured in the graph below alongside the strategy’s added value.

A somewhat unexpected behavior

For the years 2002 to 2004, our intuition seems to be validated as the hedge ratio for the US dollar (in blue) was at 60% (i.e. 10% over the benchmark) while the one for the Euro was at 0% (i.e. no hedge). This is consistent with our prior observation that the interest rate for the EUR was higher than for the USD by a margin of more than 1% (graph 2). Indeed, the strategy seems to take advantage of this situation and over-hedge the US dollar while under-hedging the Euro with respect to the benchmark. The precise levels are set so that the strategy risk still matches that of the benchmark.

However, between 2006 and 2008, the interest rate was higher for the US dollar compared to the Euro (graph 2). In such circumstances, we would expect the strategy to under-hedge the dollar and over-hedge the Euro. The hedge ratios tell another story: they have stayed at similar levels as in the 2002-2004 period where the interest rate situation was reversed. How is this possible? The answer is not featured here but can be found in the risk of the exchange rate: the 2-year volatility of the USDCHF during those years was 2 to 2.5 larger than that of the EURCHF. On top of that, remember that the US dollar exposure of the portfolio was larger by a factor of 1.5 with respect to the Euro (60% versus 40%). Consequently, the hedging cost advantage of the Euro failed to compensate for the risk stemming from the American currency and it was cheaper for the strategy to meet the risk level of the benchmark by hedging 50% to 60% of the USDCHF while leaving the EURCHF unhedged.

Where’s the risk? At this point, we must also share some concerns regarding the hedging imbalances between the two currency pairs induced by the strategy.

The real culprit

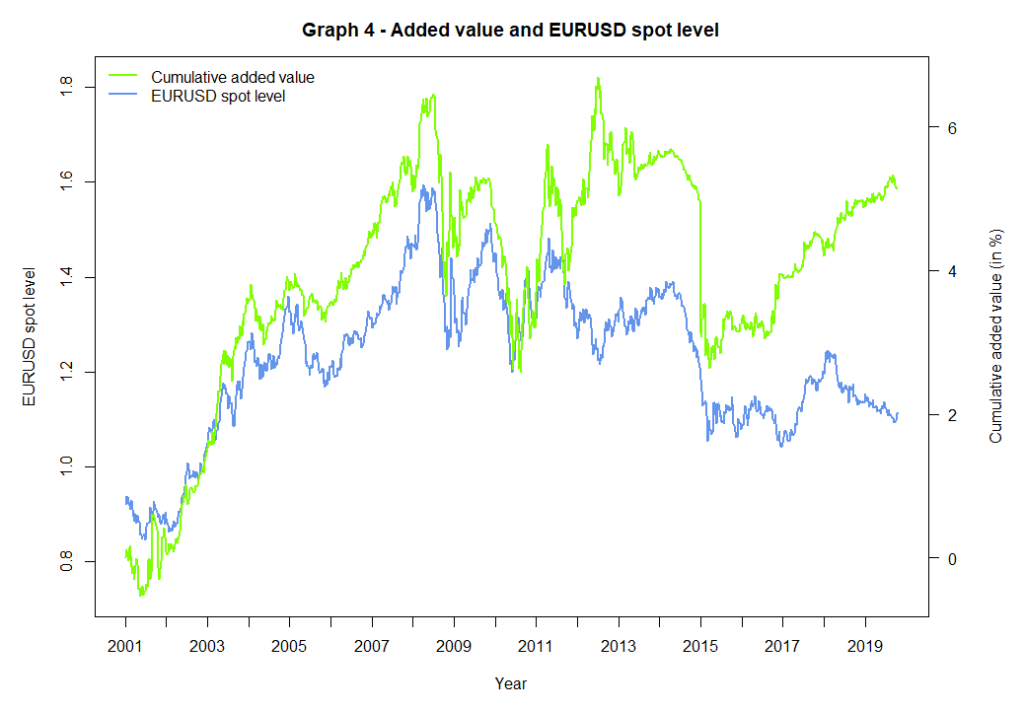

Relying on the same logic as for the interest rates, we explore the difference in variations of the USDCHF and EURCHF currency pairs directly through the trajectory of the EURUSD one. It figures in the graph below alongside the strategy’s added value.

What immediately jumps out is the tight correlation between the two curves for most of the period. Sure, the strategy is trying to profit from discrepancies in interest rate differentials but it is subjecting itself to the whims of the EURUSD exchange rate in the process. In fact, the strategy’s well-performing periods were driven in the most part by a favorable move in the EURUSD spot level: the 2002 to 2004 period is characterized by an upward move in the value of the Euro against the US dollar while the strategy under-hedges the European currency and over-hedges the American one, thereby taking advantage of the trend. This is the bright side of carry strategies: when the movement in the exchange rate expands the returns we are set to make on the interest rate differential.

Not what we were betting on

But then the winds change, as was the case between 2008 and 2010, and our implicit bet on the currency pair’s exchange rate wipes out nearly half of the gains made over the previous 8 years. Even in recent years (2017 to 2020), which presented an attractive environment for our strategy with low volatilities for both the USDCHF and EURCHF combined with a large gap in interest rate differentials between the two currency pairs, the variations in the exchange rates remain a prominent driver of performance. Indeed, the strategy is implicitly long the EURUSD (USDCHF hedge ratio stands at 50% versus 40% to 30% for the EURCHF) in 2017 and benefits from its upward trend. It then reverses its positioning (40% USDCHF versus ~80% EURCHF) between 2018 and 2020, just as the EURUSD starts heading lower.

Conclusion

Throughout this paper, we have dissected the performance and behavior of a seemingly straightforward cost-conscious hedging policy.